The second is Cash Equivalents which are investments that are short-term highly liquid and are readily convertible to. The Bipartisan Budget Act of 2015 BBA repealed the TEFRA partnership procedures including the electing large partnership provisions and replaced them with a new centralized partnership audit regime.

Audit Cash Cash Equivalents Youtube

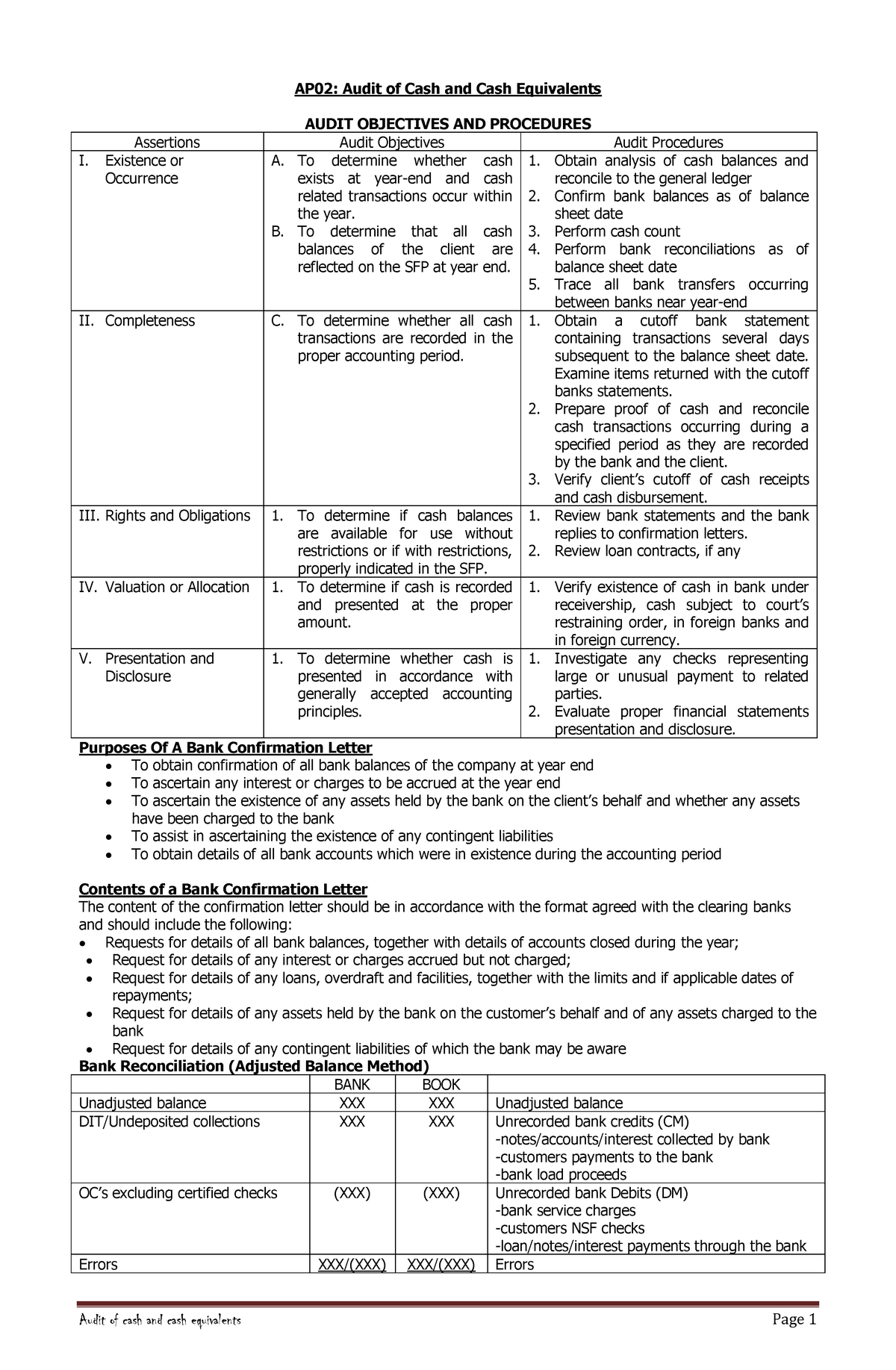

These audit procedures are given below.

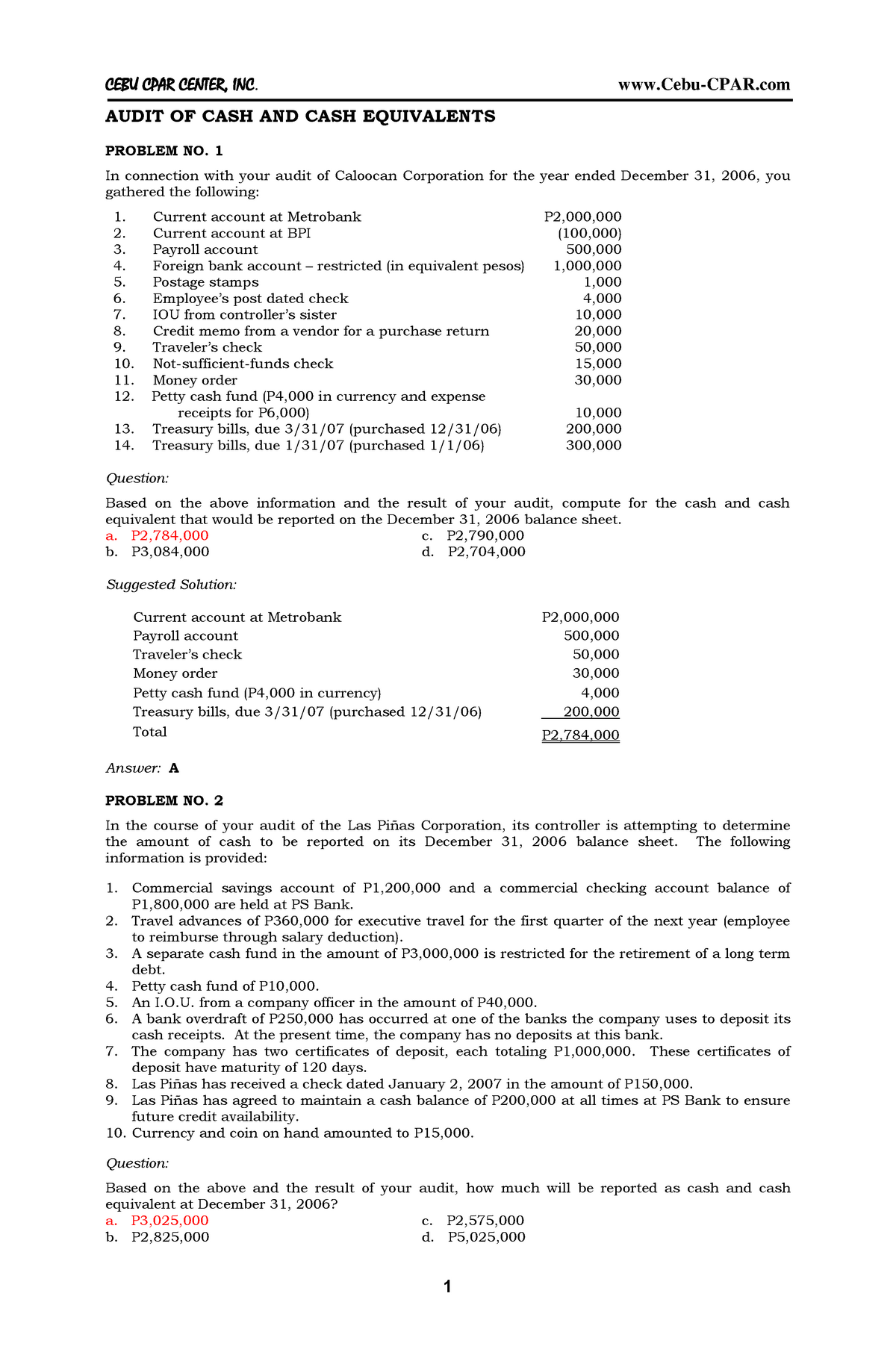

. All cash and bank audit procedures need to be properly documented and all. Properly filled out this form will satisfy the requirements of Regulations Parts 3 and 5 29 CFR. As of December 31 20X2 and 20X1 cash and cash equivalents consist of an operating checking account.

LBI Industry Guidance 04-0118-007 dated 212018 established procedures to ensure waiver requests are applied in a fair consistent and timely manner under the regulations. 2 Procedures must be implemented to control cash or cash equivalents based on the amount of the transaction. Cash control is cash management and internal control over cash.

Related article Audit Procedures for Cash and Cash Equivalents. An audit report is an independent opinion of a personfirm ie. For the seller revenue can be revised by debiting the sales return account A contra account by nature and crediting cashaccounts receivable with the invoice amount.

Whenever the circumstances warrant the Chairperson or the ClusterRegional Director may constitute special audit teams to conduct cash examination. 1 Page 1 of 17 AUD Handouts No. For taxable years beginning January 1 2018 the tax treatment of all items in a partnership return is governed by rules established by BBA.

A Form 1099 Information Return or its foreign equivalents. ASUNCION CPA MBA DEFINITION OF CASH Cash includes money and other negotiable instrument that is payable in money and acceptable by the bank for deposit and immediate credit. They will need to get idea about the number of banks types of bank accounts authorized signatories authorization matrix bank payment process petty cash payment process etc.

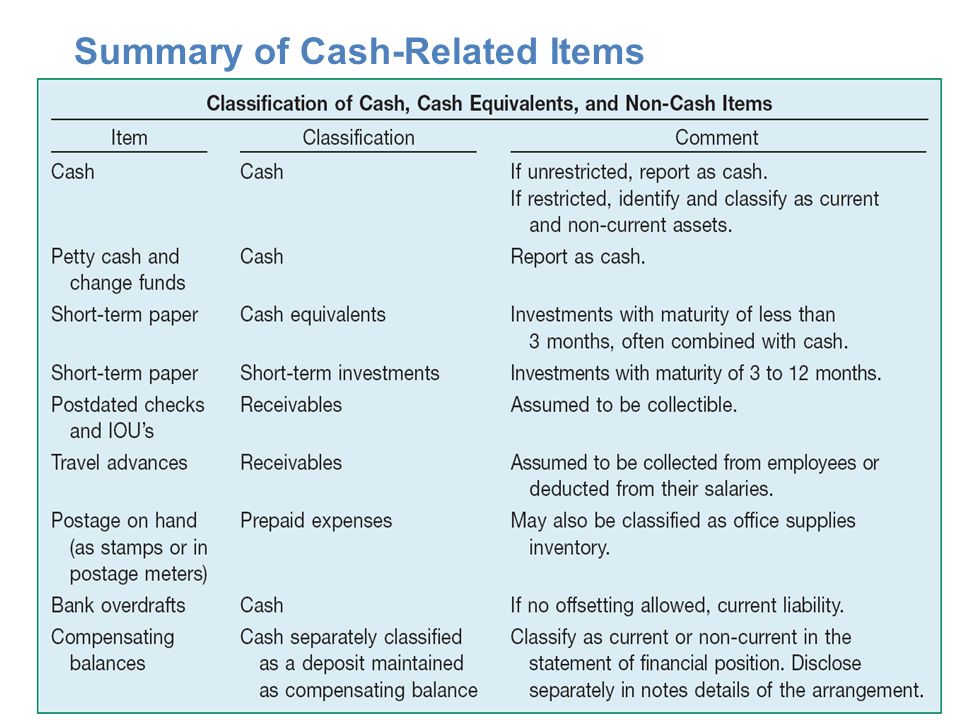

The first is cash which comprises cash on hand and at the bank. Unverified transfers of cash or cash equivalents are prohibited. This is a statement of the companys cash and cash equivalents Cash And Cash Equivalents Cash and Cash Equivalents are assets that are short-term and highly liquid investments that can be readily converted into cash and have a low risk of price fluctuation.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. Staff must review procedures annually as a refresher. Cash resources means cash in form of Bank notes or coins.

Automate processes construct unique verification flows and investigate cases in-depth all in a few clicks. Accounts Receivable Trade accounts receivable are stated net of an allowance for doubtful accounts of 7500 at December 31 20YY and 20XX. It includes cash on hand demand deposits and other items that are unrestricted for use in the current operations.

In Cash and Cash Equivalents there are two separate components. Cash equivalents are short-term balances with an original maturity of three months or less from the date of deposit highly liquid investments that are readily convertible into known amounts of cash and which are subject to insignificant risk of changes in value. Through an examination treatment stream this campaign will concentrate on bringing into compliance those.

Departmental procedures should incorporate the principles of good cash handling which include the following. IntroductionThe purpose of this handbook is to establish and document the flow of cash and cash receipts and provide guidelines for the proper management of monies for those employees responsible for receiving handling and safeguarding cash and cash equivalentsThe custodian of every cash fund is responsible for the integrity of the cash fund. The procedures selected depend on the auditors.

26 Cash flow statement Cash flows are reported using the indirect method. Auditor about whether the financial statements present a true fair view of the state of affairs of the entity profitloss of the entity cash flows for the year and such opinion is given after performing reasonable audit procedures so obtain sufficient appropriate evidence for the assurance. In addition they must review updated departmental procedures as provided by unit management in a timely manner.

These procedures must include documentation by shift session or. WH-347 PDF OMB Control No. Form WH-347has been made available for the convenience of contractors and subcontractors required by their Federal or Federally-aided construction-type contracts and subcontracts to submit weekly payrolls.

Assets and liabilities for which the turnover is quick and the maturities are three months or less such as debt loans receivable and the purchase and sale of highly liquid investments Cash Flows from Operating Activities. Cash and Cash Equivalent is scoped under IAS 7 Statements of Cash Flows. This will help the auditor to plan audit procedures for cash and cash equivalents.

Cash and Cash Equivalents for Year Ended June 30 In Thousands Carrying Amount 2012 2011 2010 Cash in bank 56362 60809 46487. 05 DARRELL JOE O. It proves to be a prerequisite for analyzing the business.

Automatically generate reports for regulators and partners. Auditing Cash and Cash Equivalents. Internal control includes corporate governance company policies segregation of duties authorized approvals for purchases designated signature authority with limits payments reconciliation and bank.

Cash Equivalents For purposes of the statement of cash flows the Company considers all highly liquid debt instruments with a maturity of three months or less to be cash equivalents. Cash purchases and sales of cash and cash equivalents. Help your team handle сompliance.

Cash and paper money US Treasury bills undeposited receipts. Account receivable or cash and cash equivalents should also affect whether it is the cash sale or credit sales. As noted in Table 2 the system had approximately 114 million in cash and cash equivalents in local bank accounts and approximately 793 million in the state treasury at June 30 2012.

Controlling cash receipts and cash disbursements reduces erroneous payments theft and fraud. Has audited Income Statement Balance Sheet Cash Flow Cash Flow Cash Flow is the amount of cash or cash equivalent generated consumed by a Company over a given period. It is really important to ensure that inventory-related measures are properly taken care of essentially because of the tantamount importance it has not only on the Income Statement but also on the Balance Sheet.

We recommend reviewing policies and procedures every January. Here we discuss Types of Audit report opinion and Sample Audit Report examples including Facebook Tesco Plc. Here is the sale return journal entry.

Of three months or less are cash and cash equivalents. Audit committee means a committee established under section19. The audit team leader shall be responsible in identifying the audit team members who will conduct or assist him in the cash examination.

Auditor-General means the Auditor-General appointed in accordance with the Constitution. Bank account means an account at a bank into which moneys are deposited and drawn.

Ap Cash Cash Equivalents Q Audit Of Cash And Cash Equivalents Problem No 1 In Connection With Studocu

Cash Audit Procedures Assertions Objectives Management Cash Exists Include All Transactions That Should Be Presented Represents Rights Of The Entity Ppt Download

How To Audit Cash And Cash Equivalents Basic Audit Procedures

Audit Of Cash And Cash Equivalents Existence Or Occurrence A To Determine Whether Cash Exists At Studocu

0 Comments